The eternal Shakespearean question “to be or not to be” in our time has transformed into the no less relevant “to buy or to rent.”

There is an opinion that real estate in Toronto is overpriced, and that renting right now is more profitable than buying something of your own.

But let me explain the opposite point of view with a specific example.

Let’s take for example a 1-bedroom apartment in Richmond Hill, specifically this one: unit 501 in the building at 51 Baffin Crt. Here is a more detailed description with photos: www.agent1.ca/51baffin

. As you can see, it is listed for sale at $448,000.

Let’s use this example to compare how profitable it is to rent or buy it, and how much money will be “thrown away” in one case or the other. This apartment is not unique — there are plenty of similar options. If you’re interested, call me — besides this one, I have plenty more examples.

Let’s fix the expenses for this apartment as of today, and for the sake of simplicity assume that expenses won’t change over the next 5 years (although of course, rent will increase, but so will property tax).

At the moment, renting such a condo will cost about $2,300 per month. That means in 5 years we will irrevocably lose 2300 * 60 = $138,000. On the plus side, renting offers flexibility and ease in the form of being able to move if needed, as well as passing all repair/maintenance issues onto the landlord (say, if a faucet leaks). But on the minus side — you may be forced to move out if you didn’t plan to: for example, if the landlord’s circumstances change and he decides to move into the unit himself. In that case you’ll have to move, your child may need to change schools, you’ll be scrambling to find another rental at a new price, and so on.

What about buying?

The irretrievably lost money in this case is property tax (~$1,700 a year, which over 5 years will amount to $8,500) and maintenance fee ($550 per month, which over 5 years turns into $33,000), plus mortgage expenses.

In addition, “irretrievable losses” include closing costs — land transfer tax, lawyer fees, and other small unpleasant expenses that can be roughly estimated at $5,000 for first-time buyers (the exact sum depends on your situation and requires clarification).

The most complicated issue, of course, is the mortgage.

The undeniable minus here is the need for a down payment, which must be made when purchasing — from 5% to 20% of the property price. 20% is preferable, since with that your mortgage won’t require adding government insurance, but with less than 20% down, having that insurance makes it a bit easier to get approved for a loan from the bank.

An important side note: not all mortgage expenses are losses. Mortgage payments include interest payments (bank interest, which is indeed irrevocably lost for us), plus principal payments, which go toward reducing your debt to the bank. The principal is not a loss — it is simply repayment of your debt, increasing your equity, i.e. your paid-off share of the property’s value.

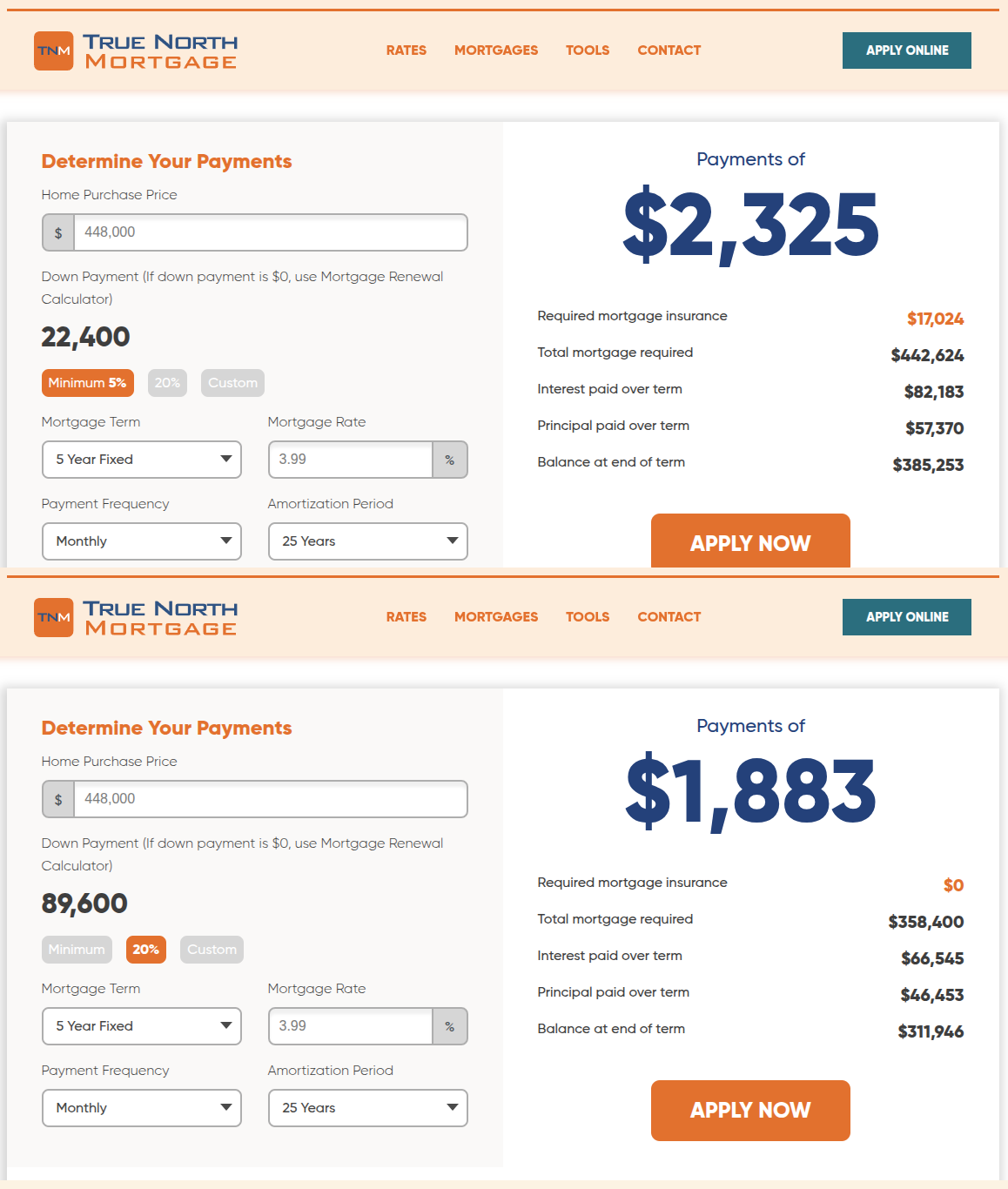

Let’s look at the screenshots attached to the listing.

One of the major players in the mortgage market, True North Mortgage, is currently offering a 3.99% fixed-rate mortgage for 5 years (believe it or not, I didn’t get a cent for this ad!). Perhaps right now it would be wiser to take a variable rate, but for the sake of predictability in our comparison let’s stick with the fixed option.

With a 5% down payment ($22,400, top part of the screenshot) you would lose $82,200 on mortgage interest over 5 years (see column “Interest paid over term”).

With a 20% down payment ($89,600, bottom part of the screenshot) you would lose $66,500 on mortgage interest over 5 years. Note that in this case you also avoid the government mortgage insurance of $17,000, which is required with only a 5% down payment.

As a result, if you have $90,000 (20%) set aside for a down payment on your own apartment (plus the mentioned closing costs), then over the next 5 years you will lose not $138,000 as in the case of renting, but only $8,500 (property tax) + $33,000 (maintenance) + $66,500 (mortgage interest) = $108,000. It may seem like only a $30,000 difference — but still, nice, isn’t it?

Yes, overall you will be paying more per month than in the case of rent, but these will not be lost rental payments or bank interest, but rather a reduction of your debt to the bank for your apartment (principal payment).

In the end, after 5 years, if you rented you’d still be at the same starting point ($138,000 gone, no property of your own, start all over again, find a new rental — but at a higher price). Meanwhile, with your own property you’d be at the point of “I have my own apartment and I owe the bank only $312,000, and from here on my payments get smaller and smaller.”

I assume that the price of this condo in 5 years will not be less than $500,000 (remember this tweet!). In that case, your equity (your financial stake in the apartment) will be at least $500,000 minus $312,000 remaining debt to the bank = $188,000. That’s twice the amount of your initial down payment. You could sell the apartment and pocket that money (minus selling expenses), if you wanted to.

If you instead use the minimum allowable down payment of 5% ($22,400, see the top part of the screenshot), then over 5 years your irretrievable losses (property tax + maintenance fees + mortgage interest) will total 8,500 + 33,000 + 82,200 = $123,700. Not such a big difference compared to the 20% down payment case, but still, the losses are $14,000 less than with renting. Plus, after 5 years you’ll still have an apartment with an assumed value of at least $500K and a remaining debt of only $385K: your $22,400 could magically turn into about $115K. Or they might not — if you instead spend the next 5 years renting.

Let me emphasize again: this apartment at 51 Baffin Crt is not some unique case; there are plenty of such opportunities. If you’re interested, I can send you other options by email.

Richmond Hill, by the way, is one of the best neighborhoods in Greater Toronto in my opinion, and right now, during a market downturn and general panic, is exactly when money is made by those who are less prone to panic.

This kind of mini-analysis is what I usually offer my clients before each purchase and even before some viewings, filtering out options that financially will not appeal to you in the long term.

If you’re interested in learning about houses or condos that fit you financially, I’d be happy to help work through all the math and see if the debits and credits line up.

So, want to see this apartment with your own eyes? www.agent1.ca/51baffin

Call me and let’s go take a look, with no obligation to buy. My phone number is in the signature below.

In which case (and for whom) renting this apartment might actually be financially preferable to buying — I’ll try to explain in the next post.

Serge Skyba

Realtor® at Realty 7 Ltd, Brokerage

serge@agent1.ca

416 305 6525